Building your own home can be a dream come true, but the cost of construction and purchasing land can be a significant hurdle. This is where you start to ask Does a construction loan extend its reach to cover land? A construction loan is a high-interest mortgage that can help finance the cost of building a property. However, it’s essential to understand what construction loans do and don’t cover and what specific requirements you need to met to qualify for this type of loan. In this blog post, we will cover what a construction loan is, what it covers, and the factors to consider when obtaining one.

As a general rule, a construction loan does not cover the cost of purchasing the land but only cover the costs of materials, labor, and permits. However, there are exceptional circumstances in which a construction loan may cover the cost of purchasing the land. For example, if the borrower already owns the land and is seeking a loan to cover the costs of construction, the lender may be willing to include the value of the land in the loan.

The reason for this is that land is considered a separate asset from the building or home being constructed on it. Additionally, the value of the land may fluctuate more than the cost of construction, making it a riskier investment for the lender.

Another option for financing the purchase of land is to obtain a land loan. A land loan is specifically designed to cover the cost of purchasing land and may be easier to obtain than a traditional mortgage loan. However, the interest rates for land loans are typically higher than for other types of loans, and the terms may be less favorable.

Alternatively, a borrower may be able to secure financing for both the land and construction costs through a single loan by obtaining a construction-to-permanent loan. This type of loan allows the borrower to obtain financing for the construction phase and then convert the loan into a traditional mortgage once the construction is complete.

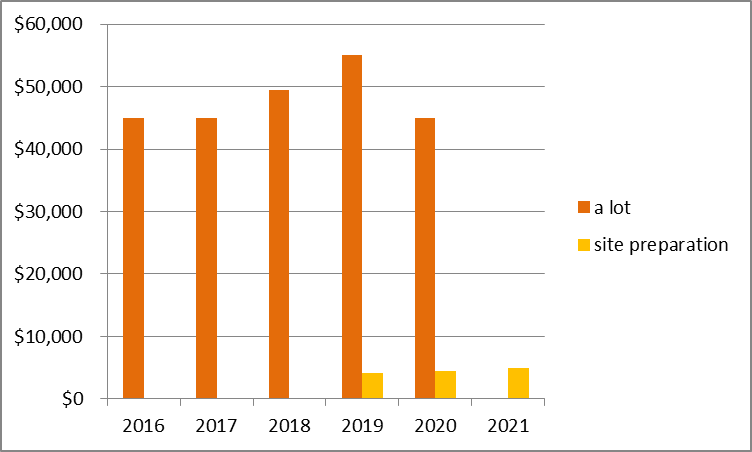

In any case, after many years in this field, I can state that the difficulty in obtaining financing for the purchase of a lot is the single most important reason why individuals choose to buy previously built houses and therefore miss the opportunity to own the house of their dreams.

What is a construction loan?

A construction loan (also known as a development loan) is a short-term, high-interest mortgage that helps finance property building. The interest rate is higher than on other loans because the investment bears a bit more risk for the lender. For example, because the home has not yet been built, the borrower may not have a home to offer as collateral. This is a bridging loan that is used to pay the expenditures of constructing new dwellings or redeveloping existing residential buildings.

There are four types of construction loans: Construction-to-permanent loan, Construction-only loan, Owner-builder construction loan and Construction Mortgage Loan.

Obtaining a construction loan typically requires meeting certain requirements. These requirements may vary depending on the lender and the specific loan product, but generally include:

- Good credit score: Lenders will typically require a good credit score to approve a construction loan. A credit score of 680 or higher you can, typically, consider as good, but some lenders may require a higher score.

- Stable income: Lenders will also want to see that borrowers have a stable source of income. This may include employment income, rental income, or other sources of regular income.

- Detailed construction plan: To obtain a construction loan, borrowers will need to provide a detailed plan for the construction project, including a budget, construction timeline, and architectural plans.

- Loan-to-value ratio: Lenders will typically require a loan-to-value (LTV) ratio of 80% or lower. This means that the loan amount cannot exceed 80% of the appraised value of the property.

- Down payment: Borrowers will typically need to provide a down payment of 20% or more of the total project cost. This down payment may need to be in cash, and you can’t finance it through the loan.

- Collateral: To secure the loan, lenders will typically require collateral in the form of the constructed property .

- Experience: Some lenders may require borrowers to have experience in the construction industry or to work with a qualified contractor.

It is important to note that these requirements may vary depending on the lender and the specific loan product. Borrowers should research different lenders and loan products to find the best fit for their individual needs and qualifications.

What does a construction loan cover?

Construction loans can be used to pay for:

- Land

- An existing property for re-development

- Permits and planning applications

- Construction materials

- Construction labor

- External services, such as architects and engineers

What factors to consider when obtaining a construction loan?

When obtaining a construction loan whether it covers the purchase of land or not, there are several important factors to consider, primarily: credit score and income requirements, interest rates and fees, and the length of the loan term.

Credit score and income requirements are important factors that lenders consider when evaluating a borrower’s eligibility for a construction loan. Generally, a higher credit score and a stable income are required to qualify for a construction loan. Lenders will also consider the borrower’s debt-to-income ratio, which compares the borrower’s monthly debt payments to their monthly income.

Interest rates and fees are also important considerations when obtaining a construction loan. The interest rates for construction loans are typically higher than those for traditional mortgage loans because they are considered higher-risk loans. Additionally, you may have to pay origination fees, closing costs, and other fees associated with the loan.

The length of the loan term is also an important factor to consider. Construction loans are typically short-term loans, with terms ranging from six months to two years. However, some lenders may offer longer loan terms, depending on the specific project and borrower’s needs.

Another important factor to consider when obtaining a construction loan is the loan-to-value ratio (LTV). This ratio compares the loan amount to the appraised value of the property. Generally, lenders will only approve loans with an LTV ratio of 80% or lower.

Finally, borrowers should also consider the lender’s experience in the construction loan market. Lenders with experience in this market may be better equipped to navigate the unique challenges associated with construction loans, such as managing construction timelines and disbursement schedules.

How to apply for a construction loan?

To apply for a construction loan, borrowers should follow these steps:

- Research lenders: Start by researching lenders that offer construction loans. Look for lenders with experience in the construction loan market and favorable interest rates and fees.

- Gather necessary documents: When applying for a construction loan, borrowers will need to provide detailed information about their income, credit history, and the project they are planning. Some of the documents required may include a detailed budget for the project, a construction timeline, and architectural plans for the building.

- Submit an application: Once borrowers have gathered all the necessary documents, they can submit an application to their chosen lender. The lender will review the application and may require additional information or documentation.

- Get pre-approved: After the lender reviews the application, they may provide the borrower with a pre-approval letter. This letter will outline the loan amount, interest rate, and other terms of the loan.

- Close on the loan: Once the borrower has found a suitable property and has a construction plan in place, they can close on the loan. At this stage, the borrower will need to provide additional documentation and sign a loan agreement.

A successful loan application includes having a clear and detailed plan for the construction project, including a budget, construction timeline, and architectural plans, and working with a lender with experience in the construction loan market. Borrowers should, of course, make sure they have a good credit score and a stable income. Once the loan is approved, the borrower can expect to receive the loan amount in installments, as construction progresses.

Construction loans are a great option for those looking to build their dream home. However, it’s important to understand that this type of loan has specific requirements, and borrowers must meet them to qualify. When obtaining a construction loan, it’s essential to consider factors like credit score and income requirements, interest rates and fees, and loan term. With the right preparation and research, borrowers can find the best construction loan for their individual needs and qualifications.